Ten questions to ask a financial planner – part one

Do you use the services of a financial planner? Have you thought about doing so but aren’t sure what – or who – you are looking for?

According to the Financial Advice Market Review around one in ten adults a year seek advice on investments, saving into a pension or retirement planning.

But as with any purchase, you need to know what you are getting for your money, so it’s important to ask the right questions before embarking on a working relationship with a financial planner.

In this blog, we look at five questions to ask, and why. In our next blog, will look at the next five:

1. What charges will be deducted from my investments?

These are the fees that you are likely to pay:

• Advice/planning fee to the adviser (for providing regulated financial advice).

• Investment platform fee (for holding your investments in one place).

• Fund manager fees (for investing your money into their fund).

Why is knowing this important?

Knowing how much you’re paying and to whom is essential for making the most of your money. Keeping costs under review is vital for long term financial success. “A penny saved is a penny earned” could not be more accurate when it comes to fees. Higher fees typically mean a bigger deduction from your investments. That’s money that your future self will not get to spend. The impact of higher fees can be staggering when compounded over time compared to lower fees.

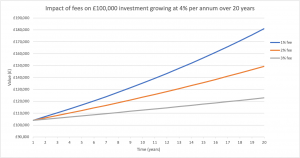

This chart shows the impact of fees (1%, 2% or 3%) on a £100,000 investment growing at 4% per annum over 20 years. The difference in portfolio value after 20 years is over £62,000!

Higher fees, when compounded over a long time, can add up to an eyewatering amount of money when compared to lower fees.

2. Do you charge fixed or percentage fees?

Percentage fees are very much the norm in financial services. A deduction is made (usually monthly) as a percentage from the assets you have invested. This means the fee you pay depends on the value of your investments. The amount you pay will increase as your investments increase in value and decease as their value goes down.

Fund manager charges are entirely percentage based. Almost all platforms charge percentage fees but some do offer tiered charges for wealthier clients. Most advisers still charge percentage fees but a few now charge fixed fees.

Fixed fees are agreed at outset and are, well, fixed. The fee doesn’t fluctuate with the value of your holdings (just like the prices of goods in shops). You don’t pay more just because you have more money.

Why is this important?

Percentage fees can be easy to understand and the numbers appear small. When framed in this way percentage fees can feel reasonable. For example, a 2% fee on £1,000,000 might seem acceptable, after all it’s only 2%. But in monetary terms it equates to £20,000.

Financial advisers are required to report initial fees and ongoing fees in monetary amounts. This means if fees are percentage based you don’t know exactly how much you are going to be charged in monetary terms.

Percentage fees mean that people with more wealth pay extra. This could lead to cross-subsidy. The fees from more profitable clients subsidise the work done on less profitable clients. The percentage fees on £500,000 are significantly higher than the percentage fees on £100,000.

Advisers who charge percentage fees will argue that higher investment values means more risk to the firm. This is true up to a point. Professional indemnity insurance and FCA fees, a requirement for all financial advisers, are calculated on turnover. But this is not your problem and is simply a feature of running a regulated financial services business.

Fixed fees ensure that everyone pays the same monetary amount for the same work. This eliminates cross-subsidy. Hence it can appear more expensive for clients with lower levels of wealth. However, fixed fees can be significantly lower than percentage fees as investment values increase.

By asking this question you are able to assess whether you are working with a firm valuing transparency and understanding around fees.

Our Answer:

Unlike most UK financial services firms we do not charge percentage fees. Instead we agree a fixed fee with you before we start. The fee reflects the work required and the complexity of your situation. We believe this is both transparent and fair. We have a structured way of calculating fees that we will share with you before we quote our fees.

3. Are you independent or restricted?

The Financial Conduct Authority has defined the terms ‘independent’ and ‘restricted’ when it comes to financial advisers. In simple terms, an independent adviser is able to recommend products from the whole of the market. A restricted adviser is only able to recommend the products from a limited number of providers.

Why is this question important?

In the past, some restricted advisers have coined hybrid terms to describe their status. Their aim is hide the fact they are restricted. This is not allowed by the FCA. The only two options are Independent and Restricted.

Restricted advisers can only recommend products from a limited number of providers. Independent advisers can recommend products from the whole of the market. Restricted advice is not bad per se, but charges can be significantly higher.

Our Answer:

We are independent. This means that we are able to advise on and recommend products from any provider right across the market. You will get the very best advice and products tailored just for you.

4. Are you registered with the FCA (Financial Conduct Authority)?

The Financial Conduct Authority is the conduct regulator for nearly 60,000 financial services firms and financial markets in the UK and the prudential supervisor for 49,000 firms, setting specific standards for 19,000 firms.

Why is this question important?

The FCA sets standards for how firms should operate and monitors them on an on-going basis. They ensure that the company or person you are dealing with has the appropriate authorisation, qualifications and resources to operate within the financial services profession.

The number of scams is on the rise. You want to make sure that when you take financial advice your adviser is regulated. This means that if something goes wrong you can make a complaint, which can be escalated to the Financial Ombudsman Service. You are also given the protection of the Financial Services Compensation scheme.

If you search the FCA Register you can find the regulatory details of the firm. We recommend you check this before commencing any work with a financial planner.

Our Answer:

Yes we are. Proposito Financial Planning Ltd is registered with reference number 572159. Huw Jones is registered with individual reference number (IRN) HRJ01006.

5. Do you offer an ongoing service and how much does it cost

Initially a financial plan is a valuable document. However, that value diminishes over time if it is not updated. An expensive financial plan, sitting on a shelf gathering dust is not much use to anyone.

Why this question is important:

If you think back to your life five years ago, it’s likely to be very different to today. On top of that, tax rules and pension legislation have changed markedly. A financial plan created back then but not updated since would be significantly less valuable.

It is essential that your plan is reviewed on an ongoing basis. It needs to evolve and adapt as things change. You need to select a planner where ongoing reviews of your plan are an integral part of their normal business operations.

If the provision of ongoing service seems uncertain or a little sketchy then you should question if that planner is right for you. The planner you choose needs to have an ongoing service that ensures your plan remains on track.

Our Answer:

People overestimate changes that will happen in the next five years but underestimate the changes over the following ten years. The real value of financial planning comes from the incremental improvements to the original plan, compounded over time.

Legislation around pensions and taxation can change quickly and often, and new opportunities arise. Your own circumstances and goals may also evolve over time.

Our ongoing LifePath Refine service is designed to make sure you remain on track to prepare for and enjoy your best retirement. We charge a fixed monthly fee that depends on the nature of the work needed to keep you on track. We will agree the ongoing fee with you when we know what you’ll need from us moving forward (after we have completed the initial financial planning work).

In our next blog, we will reveal five more essential questions to ask a financial planner, when you’re deciding who to engage for help with investments, saving into a pension or retirement planning.

In the meantime, if you would like to chat to our team you can contact us by emailing hello@proposito.co.uk or calling our Cirencester office on 01285 708444.